There is much I want to talk about. To keep the commentary concise, I plan to issue a 2-part My Gut Feeling on recent stock market and economic events.

Trumps Tariffs

To set the table, let me say a few things about the new tariffs rolled out last Wednesday by President Trump:

- We have an uneven playing field when it comes to tariffs around the world. There may be free global trade but not fair trade. This is most prominent to/from the United States. I strongly believe that this imbalance needed to be corrected and to that extent President Trump and his advisors were correct in their need to take such actions.

- I think that the roll-out of so called “Liberation Day” on April 2 (which is always a tough day on the calendar for me, as it was the day my father passed away 48 years ago) was poorly done. It was haphazard and poorly communicated.

- The tariffs on a country-to-country basis were, coming from a group of highly experienced financial and economic experts, simplistically calculated.

- We need to push out the effective dates a bit further into the future to allow negotiations to take place.

- President Trump is a negotiator and knows that you start from a position of strength and work your way from there to a final accord/solution.

What Are the United States Largest Exports?

When you see the following you might be shocked but will certainly see where the problem lies. So, we need to start and ask ourselves: What are, historically, the United States’ largest exports? It’s not cars or soybeans or pharmaceuticals or iPhones. It’s not what you think; it’s money and jobs, to put it simplistically.

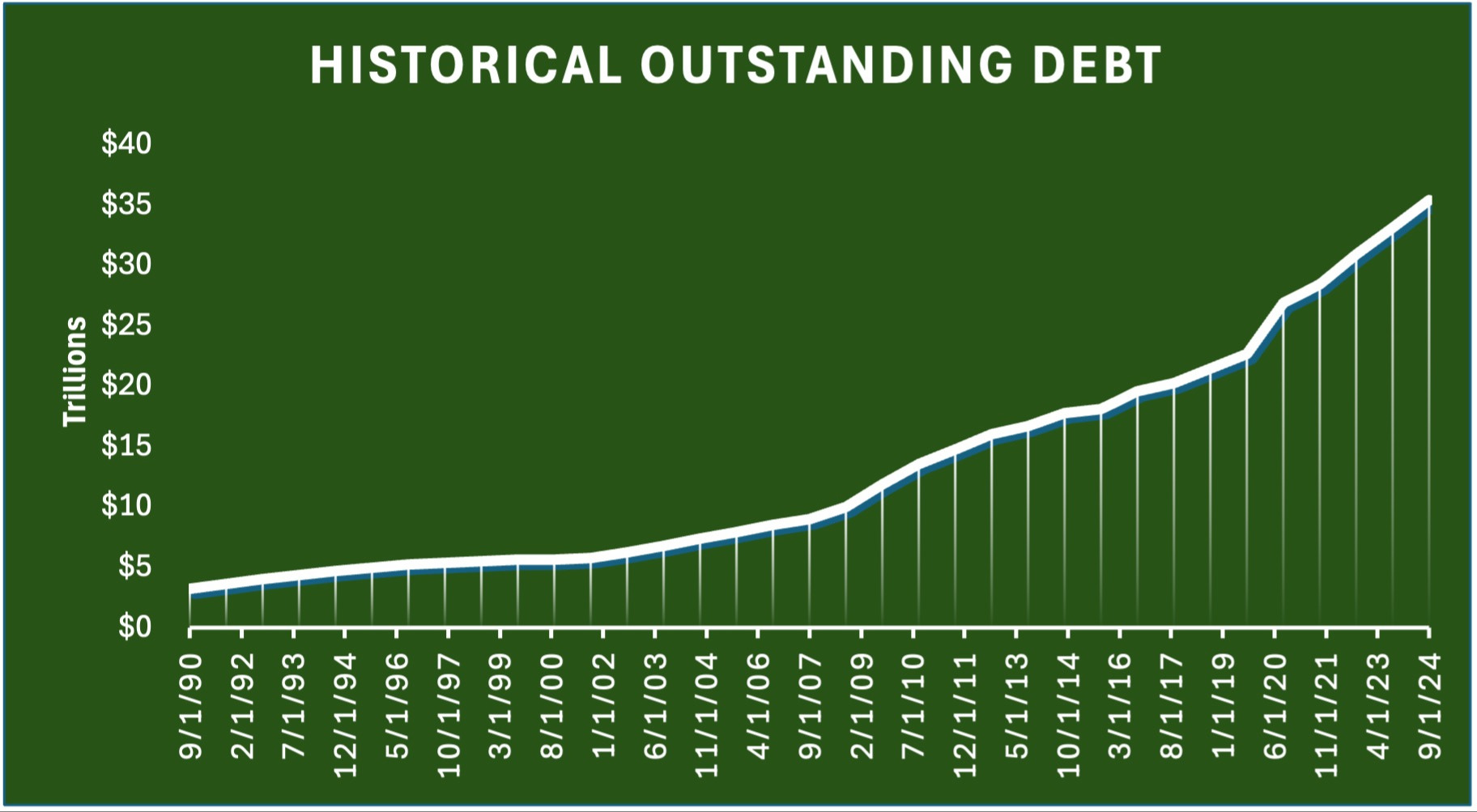

I asked Carly to help perform some research into the matter. In doing so, I went back to Adam Smith’s “The Wealth of Nations” (which I did read along with some other economic classics). Sometimes the oldies are the goodies. Specifically, we looked at two economic variables. 1. US Government Debt and 2. Manufacturing Jobs, both going back to 1990. Our sources were the US Treasury and Bureau of Labo Statistics. To save you from the tedium of the actual data Carly created two charts.

Source: FiscalData.Treasury.Gov

Since September 1990 the outstanding debt of the United States has skyrocketed from $3.233 trillion to $35,464 trillion as of September 2024. That is an annual compounded rate of 31.47%. By my estimates, about $3 trillion (plus interest) was to fix the woes of the financial crisis. Then, another $2-3 trillion was for matters related to COVID. Amazingly, in the four post-COVID years from September 2020 to September 2024, US debt surged by about $8.5 trillion due to profligate spending. Most of our $35 trillion in debt has made its way to outside of the United States by a combination of means: fighting or subsidizing foreign wars, direct aid to poorer nations, and transfer payments to American citizens who turned around and bought foreign goods (cars or stuff from Walmart (WMT) and Amazon (AMZN), for example). We need to pull this money back home to Washington to pay down our debt. There are two ways of doing so: 1. increasing tariffs and 2. eliminating waste, fraud, corruption and inefficiency in government. The latter being performed under the ‘DOGE’ effort.

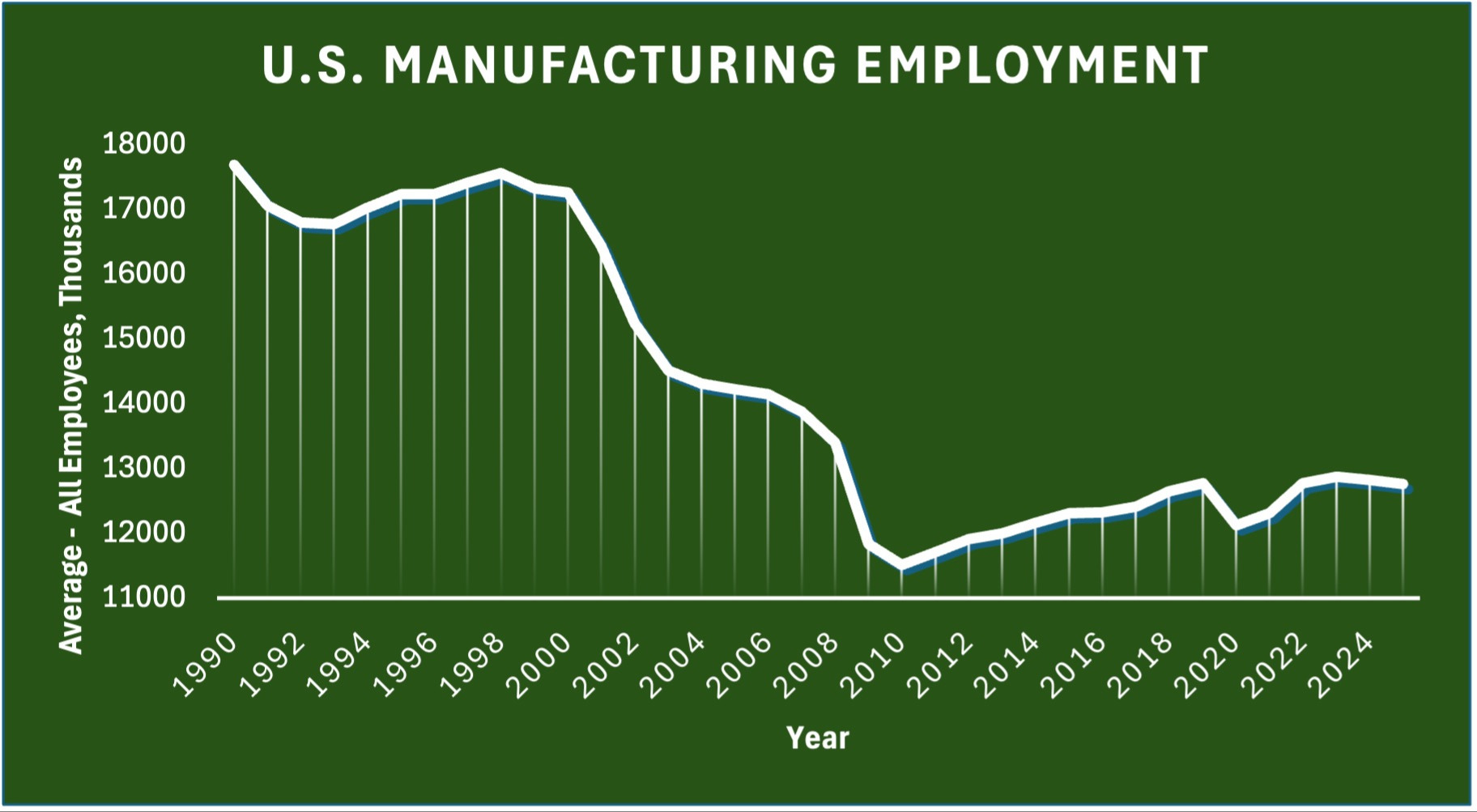

Then we looked at manufacturing jobs. According to the Bureau of Labor Statistics, manufacturing jobs at the end of 1990 stood at 17.395 million. As of March 2025, it was 13.764 million. That is a decline of 3.631 million manufacturing jobs, which is an absolute number, but when you consider economic growth over those nearly 35 years, we lost even more jobs, as we should have created more manufacturing jobs at home. That was offset by automation and technology gains.

Source: U.S. Bureau of Labor Statistics

Recall the famous interaction between the late founder of Apple (AAPL), Steve Jobs and President Obama. Obama asked what it would take to make iPhones in the United States and will they work come back home. Jobs answered that “those jobs are not coming back.”

We clearly need a manufacturing renaissance in the United States. The mistaken impression is that all products made overseas can be brought back onshore. That just won’t happen. However, there are plenty of low hanging fruit that we can bring back home. One for example is pharmaceuticals. Perhaps another is shoes and clothing.

Now repairing the two issues, debt and manufacturing jobs, is complex. We cannot afford to borrow more money to rebuild manufacturing. So, President Trump wants to get the ball rolling by having tariffs lower the debt and in turn supply capital to build factories. Then he is also convincing companies that produce overseas to invest money in building manufacturing capacity in the US. Many companies have already signed up to do so including: AAPL, Nvidia (NVDA), Taiwan Semiconductor (TSM), Oracle (ORCL), SoftBank, and Hyundai to name a few. There will be more to come. My guess is that the US Iron Dome project will be produced on home soil. This won’t happen immediately, but the sooner we get the process started, the better.

Thoughts on the Market Correction

I was in Philadelphia last weekend at a Pi Kappa Alpha Fraternity reunion. It was nice to meet and spend time with my friends, going back nearly fifty years. Many of the people there read our My Gut Feeling and My Two Cents. I was getting many questions about the market and what happens next. So, brothers, clients and readers, here it goes.

We got the correction that I was calling for. However, after the tariff announcement last week, which was an exogenous event of sorts. The correction turned into what I call, a stock version of a heart attack. I thought it was overdone, but emotions kicked in, some of it psychotic if you ask me. Now we need time to heal. Overnight it appeared as if we would have a repeat of last Thursday and Friday. Thankfully we reversed a lower open, rallied and then traded up and down as of when I wrote this My Gut Feeling, midday today, Monday April 7.

Bottoming is a process. We are beginning to see that process play out. We will have lots of market gyrations during that period of time. Some good days and some bad days will ensue. Is the worst over? I believe so. There are a few green shoots. However, we are experiencing a volatility spike. This means that professional investors and traders are bidding up the price of buying market protection (insurance) in the options market. Furthermore, the spreads in credit default swaps (another form of insurance) are being bid up. Volatility will eventually subside and when it does, markets will rebound significantly. I do not have a time and date for that to happen. Nobody will ring bells or blow horns when it happens, but there will be a lasting rebound for which we will begin another phase of the bull market.

I will work on Part 2 soon. In that I will discuss inflation, commodity prices (food and energy), The Treasury, The Federal Reserve, and have another stock market update for you.

For now, hold tight and do not make any emotional or irrational moves. As always, we are on top of client accounts and monitoring minute by minute.

______________________________________________________________________

Disclosure: At the time of this commentary Scott Rothbort, his family and/or clients of LakeView Asset Management, LLC was long AAPL, AMZN, NVDA and WMT, - although positions can change at any time. The mention of stocks are not recommendations and may not be suitable investments for your individual situation.

Scott Rothbort is the President & Founder of LakeView Asset Management, LLC, (LVAM) an investment advisor representative, specializing in high-net-worth private wealth management. LVAM is a separate entity of Osaic Advisory Services, LLC, a registered investment advisor.

For more information on investing with LakeView Asset Management, LLC call us at 702-749-9343 or request more information by clicking on the contact button on the top right-hand corner of the website or by emailing Scott at scott@lakeviewasset.com or Carly at carly@lakeviewasset.com. LakeView Management, LLC is a Nevada LLC, with its principal office located in Henderson, NV and branch office located in Millburn, NJ

© 2025 LakeView Asset Management, LLC. All rights reserved.